Do you need to get a consumer debt but find it challenging to get approved? Then presenting your car as collateral might be an option. This will help you get more favorable terms and lower interest rates with many lenders.

These transactions are possible when you have enough vehicle equity or have already fully paid your mortgage. However, you need to be aware of the potential downsides of these kinds of financing and make sure that you can afford the payments or risk your car in the process.

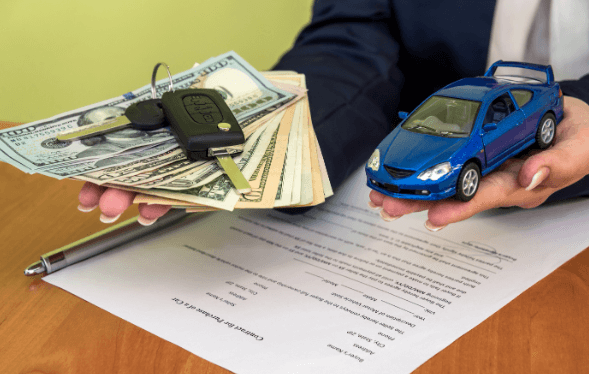

Is it Possible to Use the Vehicle as Collateral?

Yes. Many banks and financiers accept different types of vehicles when the borrower requests a consumer loan med sikkerhet. With the right lenders, you can pre-qualify for a consumer debt in minutes, and the APR can be as low as 0% when you have SUVs, trucks, and other selected vehicles. They might prefer newer cars, but used ones are also accepted as long as they meet the requirements. Shop around and know your options before signing an agreement with a lender to ensure you get the best deals. There are adjustments on the term length, down payment, brokerage costs, transaction fees, and variable interest rates that you need to know about, so ask questions before you sign on the dotted line.

For some, presenting collateral is the only way for them to get a higher amount. This is specifically for those with a bad credit rating, which is an increased risk in the eyes of many financiers. In exchange, they can get more favorable terms and lower annual percentage rates when they have something valuable to pledge. However, failure to pay the monthly due amount and to default on the agreement can mean repossession of your most valued asset.

About the Equity

Equity is the percentage of your possession of the vehicle. This is the primary difference between the amount you still owe and the collateral. Specifically, when the re sale value is at $5,000, and you still owe $2000 to the dealership, then your equity is $3,000. It’s considered a positive because the vehicle’s valuation is way more than the amount you’re requesting to borrow. The more equity you have with a newer model, the higher the chance you’ll get a reasonable interest rate.

However, there’s a risk on these equity loans because if you can’t pay for a long time and your account is past due, the vehicle will be repossessed by banks, credit unions, or private lenders so they can recoup some of their losses. Fees charged by collections and lawyers might also apply, so it’s more expensive if you can’t pay the loan.

What are the Benefits of Using a Collateral?

Get Easily Qualified for a Debt: Need a lot of funds for your daily needs, emergency expense, groceries, or to pay other loans? Getting approved for a higher amount that requires collateral can be an option. Presenting a valuable asset will help with your application, and you don’t have to look for a co-signer to qualify for a loan.

Have Lower APR: The secured debts have lower interest rates, which means you can save more money over the long run.

Any Drawbacks to Know About?

Although you’ll get fast approval for a higher amount, which is appealing for individuals who need cash soon, some risks should be considered. Some of them are the following:

Get Negative Equity – When things don’t go your way and the valuation of the vehicle decreases, there’s a huge chance that you might end up with negative equity. Getting a loan on top of your current mortgage payments means that you’re adding to your payables each month, and this can spell trouble if you can’t afford to pay everything at the end of the month.

Repossession – There are some risks of getting your vehicle seized by financiers, which is very inconvenient for those relying on their car for their daily commute to work. Aside from a chance of bankruptcy, your credit rating might get a negative hit, and you’ll find it challenging to apply for a loan in the future.

What are the Requirements?

The first thing that you need to do is to sign up for an application form on the lender’s website or call them to inquire. Generally, you must present IDs, tax returns, income, business documents, bank statements, and vehicle registration. There’s also a need to verify the collateral’s history and unit inspection that an underwriter from the bank or a private financing company will do.

Others don’t have restrictions or appraisals and are not too particular about the car’s age and mileage. The amount can be from $2,000 to $50,000 depending on the lender and the borrower’s creditworthiness, and the funds can be transferred almost immediately to a nominated bank account within the day.

The title of the car will allow a consumer debt that’s about 50% of the vehicle’s value. These are high-stakes because they need to be repaid for a short term, and some have extremely high APR of nearly 400%. Many loan sharks in the industry offer these, so you need to be careful when shopping around.

The equity and the car title type of collateral are two different things, where the former has a longer repayment length and lower interest. If you only opt for a smaller amount, presenting the title as collateral might be a good option, but the fees and the shorter timeframe can be troublesome for many people who can’t meet the payments when they are due.

If you want to avoid using your vehicle as collateral, you can also try your savings account for passbook loans available in many credit unions. You can also get a home equity line of credit if you need funds for renovations and other expenses as they can also provide you a higher amount for expensive purchases or new appliances. Just make sure that you only borrow what you can afford to pay.